Homeowners often look for ways to access the value built up in their property. Two common options are a home equity loan and a home equity line of credit (HELOC). Both allow you to borrow against the equity in your home, but they work in different ways and serve different financial needs.

Understanding the differences between these two options can help you choose the right borrowing method for home improvements, debt consolidation, education expenses, or other major financial needs.

What Is Home Equity?

Before comparing these loan options, it is important to understand home equity.

Home equity is the difference between:

The current market value of your home

The remaining balance on your mortgage

Example:

Home Value

Mortgage Balance

Home Equity

$400,000

- $250,000

- $150,000

- In this example, the homeowner has $150,000 in equity that may be used as collateral for borrowing.

- Most lenders allow homeowners to borrow up to 80–85% of their home’s value, depending on credit score and income.

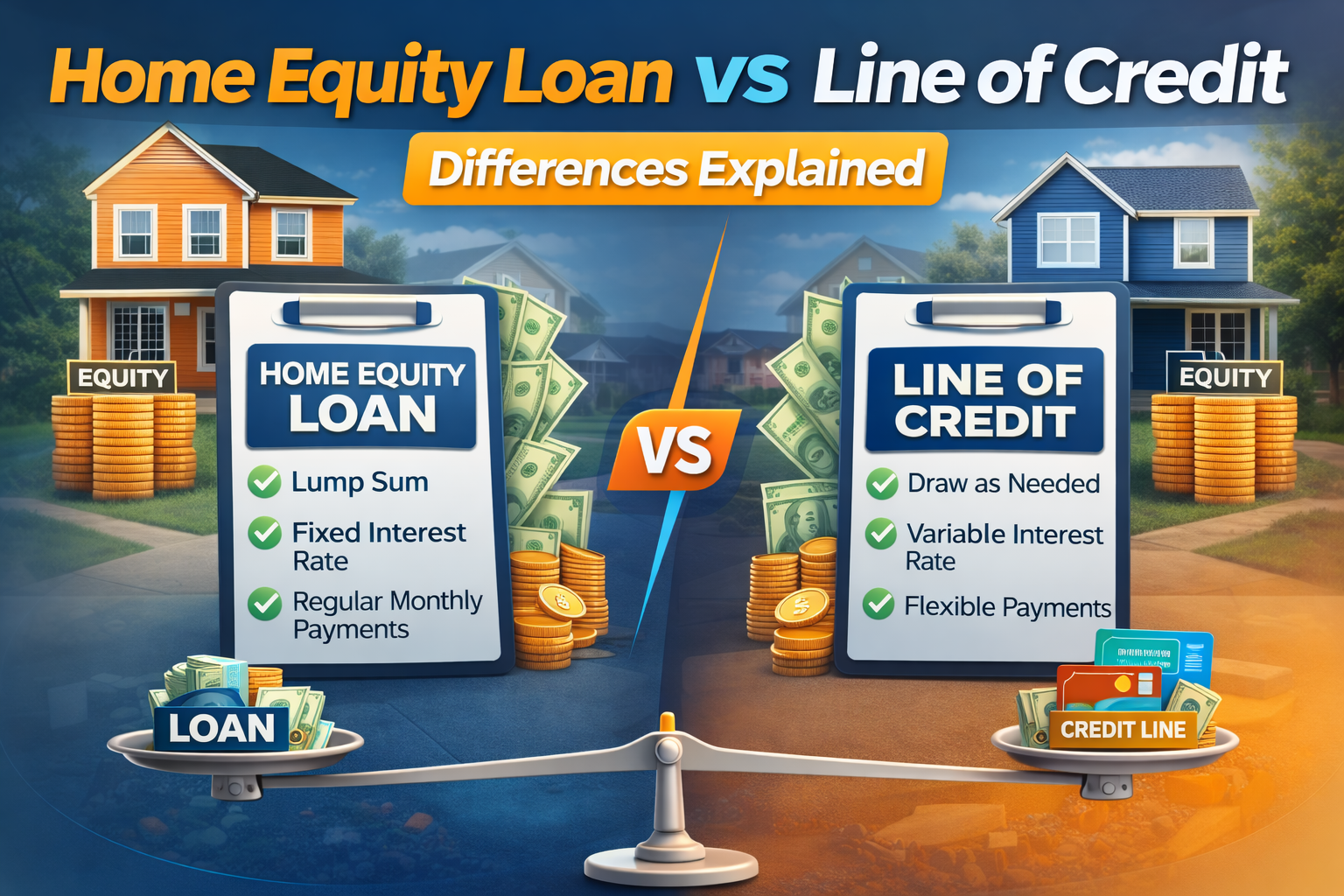

What Is a Home Equity Loan?

A home equity loan is a type of loan where you receive a lump sum of money upfront. It works similarly to a traditional loan with fixed repayment terms.

Key Features

Borrow a single lump sum

Fixed interest rate

Fixed monthly payments

Typical repayment terms: 5–30 years

Because the interest rate is fixed, your monthly payment remains stable throughout the life of the loan.

Example

If you borrow $50,000 with a 10-year home equity loan, you will receive the entire $50,000 at once and repay it with fixed monthly payments.

Advantages

Predictable monthly payments

Fixed interest rate protection

Good for large, one-time expenses

Disadvantages

Less flexibility after receiving the funds

Interest charged on the entire loan amount

Home equity loans are often used for major expenses like home renovations or debt consolidation.

What Is a Home Equity Line of Credit (HELOC)?

A home equity line of credit (HELOC) works more like a credit card. Instead of receiving money all at once, you receive a credit limit that you can borrow from when needed.

Key Features

Revolving credit line

Borrow money as needed

Variable interest rates

Draw period usually 5–10 years

During the draw period, borrowers can withdraw funds multiple times and often pay interest only on the amount used.

Example

- If you have a $50,000 HELOC, you can withdraw:

- $10,000 today

- $5,000 next month

- $15,000 later

- You only pay interest on the amount you actually borrow.

Advantages

- Flexible borrowing

- Interest charged only on used funds

- Useful for ongoing expenses

Disadvantages

- Variable interest rates may increase

- Payments may rise if rates go up

- HELOCs are commonly used for home improvements, education expenses, or ongoing projects.

Key Differences Between Home Equity Loans and HELOCs

Feature

Home Equity Loan

HELOC

Loan structure

- Lump sum

- Revolving credit line

- Interest rate

- Usually fixed

- Usually variable

- Monthly payments

- Fixed

- May change

- Flexibility

- Less flexible

- Highly flexible

- Best for

- Large one-time expenses

- Ongoing or unpredictable expenses

- The main difference is how the money is accessed and how interest is calculated.

Interest Rates Comparison

Interest rates vary depending on the lender and credit profile.

Typical ranges include:

Loan Type

Interest Rate Range

Home equity loan

7% – 12%

HELOC

7% – 13% (variable)

Because HELOC rates are variable, payments may increase if market interest rates rise.

When a Home Equity Loan Is Better

A home equity loan may be the better option if:

You need a large lump sum of money

You prefer predictable monthly payments

Interest rates are low and you want to lock them in

You are financing a specific project or major expense

This loan is ideal for homeowners who want stability and clear repayment terms.

When a HELOC Is Better

A HELOC may be the better option if:

You need flexible access to funds

Your expenses will occur over time

You want to borrow only what you need

You can manage potential interest rate changes

HELOCs are especially useful for long-term projects like home renovations where expenses occur gradually.

Risks of Borrowing Against Home Equity

Both home equity loans and HELOCs use your home as collateral. This means the lender can potentially foreclose on your property if you fail to repay the loan.

Other risks include:

Rising interest rates (for HELOCs)

Overborrowing

Increasing total debt

Borrowers should carefully evaluate their ability to repay before using home equity.

Tips Before Choosing a Home Equity Loan or HELOC

Before applying, consider the following:

- 1. Check your credit score

Higher scores usually qualify for lower interest rates. - 2. Compare lenders

Different banks offer different loan terms and fees. - 3. Understand repayment terms

Know how long the draw period and repayment period last. - 4. Borrow responsibly

Only borrow what you truly need. - These steps help ensure that borrowing against home equity remains financially manageable.

Conclusion

Both home equity loans and HELOCs allow homeowners to access the value built up in their property. However, they work differently and serve different financial needs.

Home equity loans provide a lump sum with fixed interest rates and predictable payments.

HELOCs offer flexible borrowing with variable interest rates and revolving credit access.

The best option depends on your financial goals, spending needs, and comfort with interest rate changes. By understanding these differences, homeowners can make informed decisions and use home equity wisely.

FAQs

1. Is a HELOC better than a home equity loan?

It depends on your needs. HELOCs are more flexible, while home equity loans provide fixed payments and stability.

2. Can I use a HELOC for any purpose?

Yes. Many homeowners use HELOC funds for renovations, education, or debt consolidation.

3. What credit score is needed for home equity loans?

Most lenders prefer a credit score of 620 or higher, though better rates are offered above 700.

4. Do home equity loans have fixed interest rates?

Yes. Most home equity loans come with fixed interest rates.

5. What happens if I cannot repay a home equity loan?

Because the loan is secured by your home, the lender may start foreclosure proceedings if payments are missed.